If you’ve ever opened a bank account, used a debit or credit card, taken a loan, or invested in stocks, you’ve already been using TradFi even if you didn’t know the name for it.

TradFi, short for Traditional Finance, is the long-established financial system that manages money, assets, and investments through centralized institutions. It’s the system most of the world has relied on for decades (and in many cases, centuries). While newer models like DeFi aim to disrupt it, TradFi still runs the global economy behind the scenes.

The Core Idea of TradFi

TradFi is built on trust in institutions.

Instead of individuals handling financial transactions directly with one another, TradFi relies on intermediary banks, exchanges, and regulators to manage money and enforce rules. These institutions verify identities, record ownership, process payments, and step in when things go wrong.

This structure didn’t appear randomly. It developed over time as trade expanded and economies became more complex. Governments and financial authorities added regulations to reduce fraud, prevent crises, and protect everyday users.

The result is a system that prioritizes stability, predictability, and legal protection, even if that sometimes comes at the cost of speed or flexibility.

Main Features of TradFi

Traditional finance has a few defining characteristics that shape how it operates:

- Centralized control

Financial institutions and authorities make key decisions and manage infrastructure. - Mandatory intermediaries

Most transactions pass through banks, brokers, or payment processors. - Strict regulation

Governments enforce rules to protect consumers and markets. - Identity-based access

Users must verify who they are to use financial services. - Established processes

Systems are reliable but slow to change.

These traits explain why TradFi feels familiar and secure but also why people sometimes find it restrictive.

Key Players in the TradFi System

TradFi works because many different institutions interact with each other. Each one plays a specific role.

Commercial banks

These are the most visible part of TradFi. They accept deposits, provide loans, process payments, and offer everyday financial services to individuals and businesses.

Investment banks

Investment banks handle large-scale financial activity. They help companies raise capital, manage mergers, and operate in global markets.

Central banks

Central banks manage national monetary systems. They control money supply, set interest rates, and intervene during financial crises to stabilize economies.

Asset managers and institutional investors

These firms manage pooled money from individuals, pensions, and institutions, investing it across markets to grow wealth while managing risk.

Regulators and supervisors

Regulatory bodies create and enforce the rules. They monitor institutions, promote transparency, and protect consumers from fraud or abuse.

Together, these players keep the financial system running even if most users never see what’s happening behind the scenes.

How TradFi Works in Real Life

TradFi is so embedded in daily life that it’s easy to forget how complex it really is.

When you get paid, your salary moves through banking networks. When you pay with a card, payment processors, banks, and clearing systems communicate instantly. When you invest, brokers, exchanges, custodians, and settlement systems all play a role.

Behind even simple actions are layers of infrastructure:

- Payment networks that move money

- Clearing systems that confirm transactions

- Settlement systems that finalize ownership

- Custodians who safeguard assets

This complexity is intentional, it reduces risk and creates accountability at every step.

Financial Products You See in TradFi

Traditional finance offers a wide range of familiar financial tools, including:

- Savings and checking accounts for daily money use

- Loans and mortgages for personal and business needs

- Stocks and bonds for investing

- Derivatives for managing or taking on risk

- Insurance products for protection against uncertainty

These products may seem basic compared to crypto innovations, but they’re backed by legal systems and long-standing market practices.

The Role of Regulation in TradFi

Regulation is central to how TradFi operates. It exists to keep the system stable and protect users.

Regulators focus on things like:

- Preventing fraud and market manipulation

- Ensuring institutions hold enough capital

- Protecting consumers and investors

- Reducing systemic risk during economic stress

The upside is trust and legal protection. The downside is higher costs, slower innovation, and barriers for smaller players.

Strengths of TradFi

Despite criticism, TradFi has some clear advantages:

- High stability built over time

- Strong consumer protection through laws

- Clear accountability when problems occur

- Easy-to-use systems most people already understand

- Deep global integration across markets and countries

For users who value safety and predictability, these strengths matter a lot.

Where TradFi Falls Short

TradFi also has limitations that are becoming more obvious in a digital world:

- Transactions can be slow and costly

- Access may be limited by location or documentation

- Innovation moves cautiously

- Centralized control creates single points of failure

- Many people remain underbanked or excluded

These weaknesses are exactly why alternative systems have gained attention.

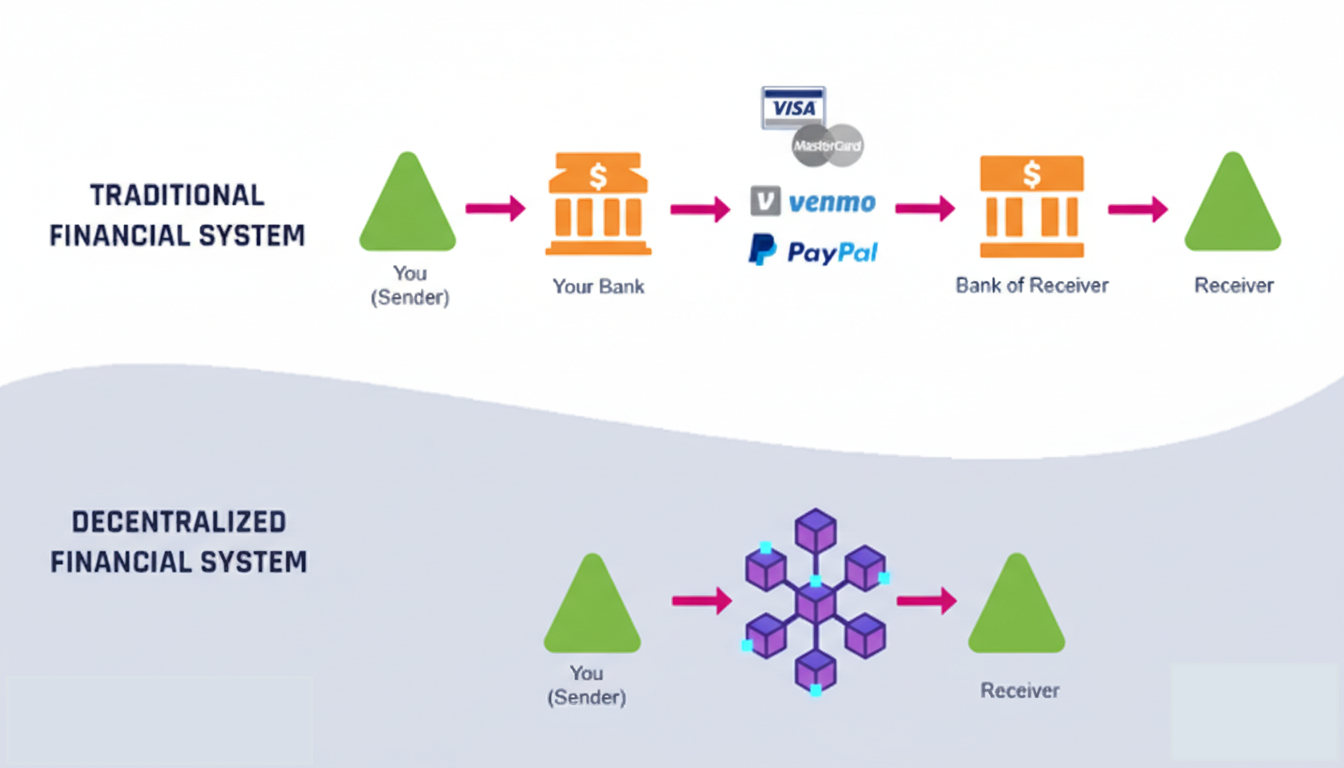

TradFi vs DeFi: A Clear Comparison

To understand TradFi better, it helps to compare it directly with decentralized finance.

| Feature | TradFi (Traditional Finance) | DeFi (Decentralized Finance) |

| Control | Centralized institutions manage funds | Users control their own assets |

| Intermediaries | Banks, brokers, payment processors | Smart contracts replace intermediaries |

| Regulation | Strict and enforced by governments | Limited or still evolving |

| Accessibility | Often restricted by geography and paperwork | Open to anyone with internet access |

| Transaction Speed | Can take hours or days | Often near-instant |

| Transparency | Low systems are mostly private | High activity is public on blockchains |

| Risk Profile | Lower but tied to institutions | Higher due to code and market risks |

| User Experience | Familiar and beginner-friendly | Requires technical understanding |

This table highlights why neither system is “perfect”; they simply prioritize different values.

The Future of TradFi

TradFi isn’t disappearing. Instead, it’s adapting.

We’re already seeing:

- Banks are experimenting with blockchain infrastructure

- Tokenization of real-world assets

- Hybrid platforms mixing compliance with crypto tech

- Regulators creating clearer rules for digital assets

Rather than competing head-on, TradFi and newer systems are starting to overlap.

Foundation of Finance

TradFi may not be flashy, but it’s still the backbone of global finance. It supports economies, protects consumers, and moves massive amounts of value every day. While it has flaws, especially around speed, access, and cost, it also offers stability that newer systems are still working toward.

Understanding TradFi helps you see the bigger picture. Whether you’re exploring crypto, investing traditionally, or just managing everyday money, knowing how traditional finance works gives you a stronger foundation to navigate the future of finance.