Think of a busy farmers’ market. If no one brings products, shoppers leave. Markets need inventory. In finance and crypto, the people (or algorithms) that bring inventory assets ready to buy or sell are called liquidity providers (LPs). They make trading possible, reduce wait times, and help buyers and sellers find fair prices.

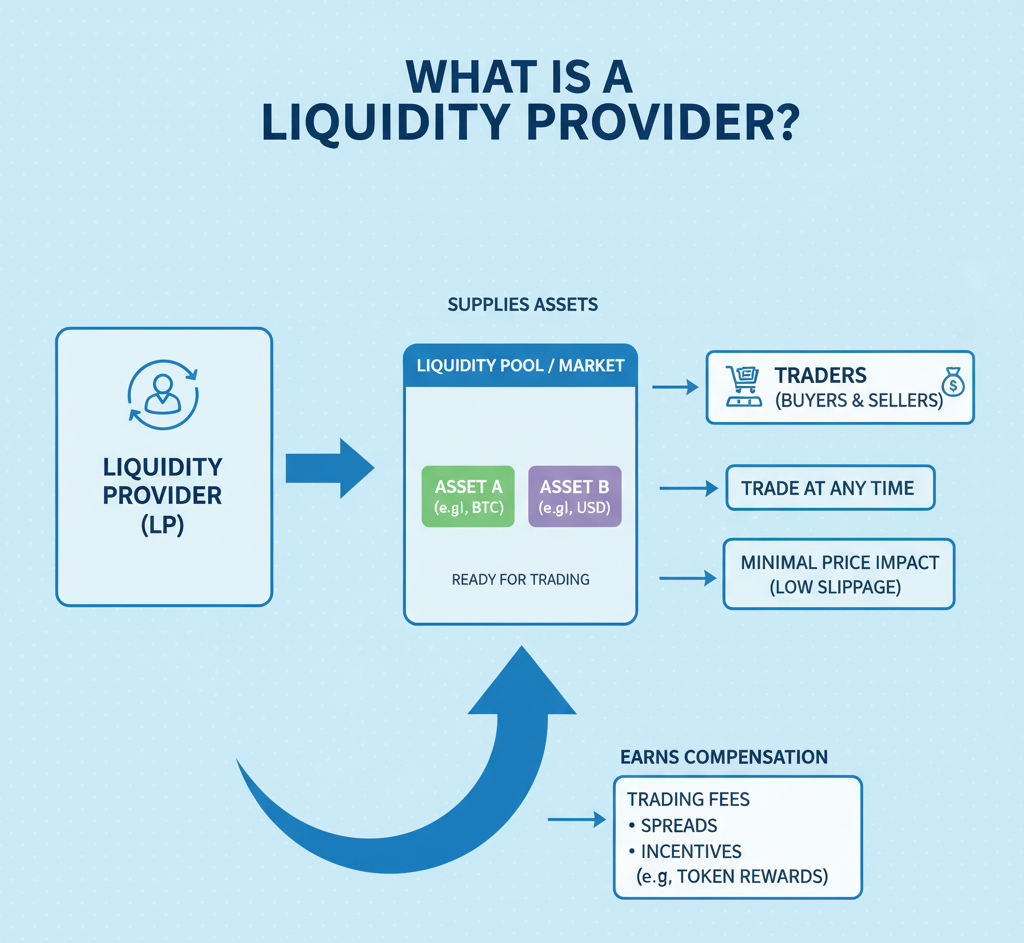

What is a Liquidity Provider?

A liquidity provider supplies assets to a marketplace so others can trade at any time with minimal price impact (low slippage). In return, LPs earn compensation fees, spreads, and sometimes incentives (token rewards).

- In traditional markets (order books), specialist firms (market makers) continuously quote bid (buy) and ask (sell) prices. They keep an inventory and profit from the spread and rebates while managing risk with hedging.

- In crypto (AMMs/DEXs): anyone can become an LP by depositing two (or sometimes one) assets into a liquidity pool. Traders swap against that pool and pay a fee; fees are distributed to LPs pro rata.

Why Liquidity Matters

- Tight spreads & fair prices: more liquidity = smaller gaps between bid/ask, which means better prices for everyone.

- Lower slippage: large orders move the price less in deep pools.

- Faster execution: you don’t wait for a counterpart; liquidity is already there.

Without liquidity providers, markets feel empty: prices jump around, trades fail, and confidence erodes.

Two Core Models

1) Order-Book Market Making (CEXs, TradFi)

- How it works: LPs place limit buy/sell orders around the current price, updating them rapidly as the market moves.

- Revenue: the spread, exchange rebates, and sometimes maker incentives.

- Risks: inventory risk (price moves against you), adverse selection (trading against informed flow), and technology/latency costs.

2) AMM Liquidity Provision (DEXs)

- How it works: LPs deposit assets into an automated market maker (AMM). The pool’s formula (e.g., constant product x·y=k) sets prices based on the ratio of assets.

- Revenue: trading fees (e.g., 0.05%–1% per swap depending on the pool), plus optional liquidity mining rewards.

- Risks: impermanent loss (IL) (explained below), smart-contract and oracle risk, L1/L2 congestion and gas costs, and MEV (front-running or sandwich attacks that can reduce fee capture).

Key Terms

- TVL (Total Value Locked): how much capital sits in a pool useful proxy for depth and trust.

- Fee tier: the percentage fee charged to traders; higher tiers compensate LPs for more volatile pairs.

- Slippage: how far the execution price moves from the quoted price due to trade size and depth.

- LP tokens/positions: receipts for your share of the pool; you burn or remove them to withdraw.

- Concentrated liquidity: provide liquidity only in a chosen price range (e.g., Uniswap v3). This increases fee earnings per dollar but requires active management.

- MEV (Miner/Validator Extractable Value): Bots or validators reorder transactions to profit, causing worse prices, slippage, or reduced earnings for users.

- Impermanent Loss (IL): Temporary loss when asset prices diverge inside a pool. Realized only when liquidity is withdrawn; common in volatile markets.

- L1/L2 Congestion & Gas Costs: Network traffic increases fees and slows transactions, affecting trade execution or liquidity adjustments.

- Oracle Risk: Risk that faulty or manipulated data feeds cause incorrect pricing, trades, or liquidations.

How LPs Earn

- Trading fees: your primary revenue stream; paid in proportion to your share of the pool and the time you’re active in the range.

- Incentives: some protocols distribute extra tokens to LPs (emissions).

- Spread capture (order books): CEX/TradFi market makers earn by buying slightly below and selling slightly above the market.

Rule of thumb: Higher fees and more volume generally mean more revenue but also come with higher volatility and inventory risk.

Impermanent Loss (IL)

Impermanent loss is the difference between HODLing the assets versus providing them to a pool when prices diverge.

- Example: You provide $5,000 in ETH and $5,000 in USDC to a 50/50 pool. ETH doubles. As traders arbitrage the pool, you end up holding less ETH and more USDC than if you had just HODLed. Your pool position is still worth more in USD, but worth less than HODLing.

- Fees can offset IL. Stable-stable pools (USDC/USDT, stables/LSTs) have low IL; volatile-volatile pairs (ETH/ALT) have higher IL.

Concentrated liquidity magnifies both outcomes: higher fee capture if trades occur inside your range, but you earn nothing (and face IL) when the price exits your range until you rebalance.

Variants You’ll See in DeFi

- Constant product AMMs (x·y=k): popular for volatile pairs (e.g., Uniswap v2 forks).

- Stable-curve AMMs: optimized for correlated assets (e.g., USDC/DAI); very low slippage, minimal IL.

- Concentrated liquidity AMMs: granular price-range LPing (e.g., Uniswap v3/v4, Algebra/Arrakis/Slipstream).

- Single-sided/covered LP: some protocols let you deposit one asset; internally, they mint or borrow the pair (often with added risk).

- Meta-pools & weighted pools: Balancer-style pools with non-50/50 weights (e.g., 80/20) to skew exposure.

Risks to Respect

- Smart-contract risk: bugs or exploits in pool or token contracts.

- Oracle/price risk: Manipulated or delayed prices can harm pools with external oracles.

- Regulatory & counterparty risk: jurisdictional issues; centralized operators on bridges or L2 sequencers.

- MEV & sandwiching: can reduce fee revenue or cause worse execution in volatile moments.

- Concentration risk: if one token rug-pulls or depegs, the pool can be left holding “bad” inventory.

- Tax: fee income and token rewards may be taxable; IL can complicate accounting. (Consult a professional in your jurisdiction.)

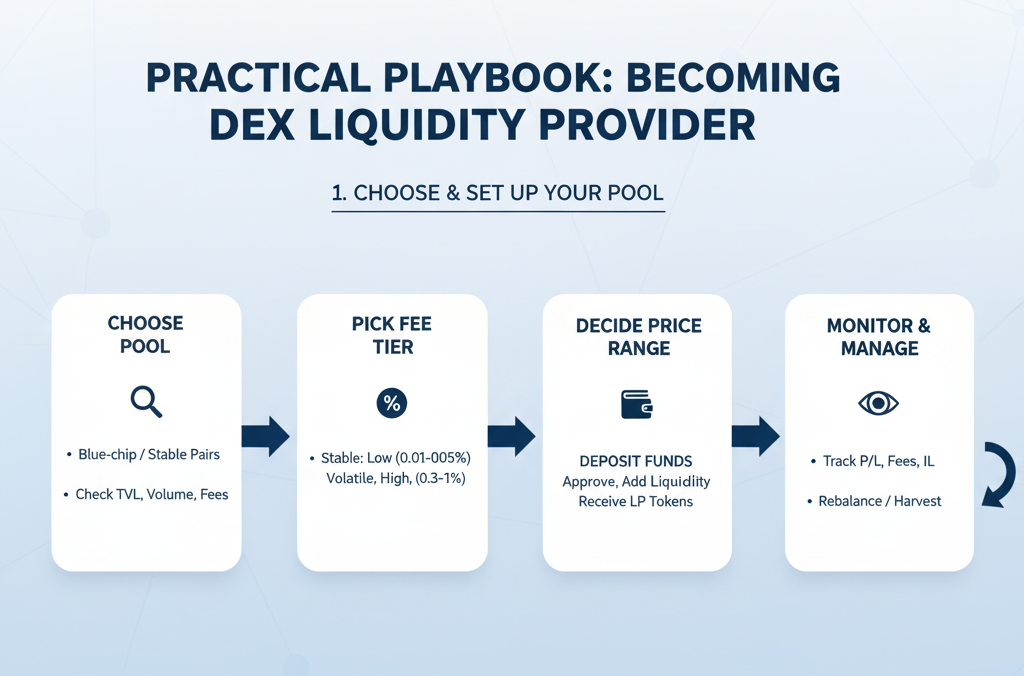

A Practical Playbook: How to Become an LP on a DEX

- Choose your pool

- Start with blue-chip or stable-stable pairs to learn mechanics.

- Check TVL, recent volume, and historical fees (fees/TVL gives a rough yield proxy).

- Pick your fee tier or pool type

- Stable pairs: lower fee tier (e.g., 0.01%–0.05%).

- Volatile pairs: higher tier (e.g., 0.3%–1%) to compensate for IL.

- Decide on price range (if concentrated)

- Wide range: easier set-and-forget, lower capital efficiency.

- Narrow range: higher fee density, but you must rebalance if price moves out of range.

- Deposit funds

- Approve tokens, add liquidity, receive LP tokens/position NFT.

- Keep small buffer for gas; consider MEV-resistant routers when available.

- Monitor and manage

- Track P/L, uncollected fees, % time in range, and IL estimates.

- Rebalance ranges after big moves; harvest fees periodically.

- Hedging (optional)

- Use perps/options to hedge directional exposure (e.g., short a portion of the more volatile asset).

- Hedging costs reduce net yield but can tame IL.

- Exit

- Burn LP tokens/close position, withdraw underlying assets + fees.

- Be mindful of exit gas and any lockups or reward-vesting schedules.

How to Evaluate a Pool (Checklist)

- Depth & volume: Deep TVL with steady daily volume is ideal.

- Fee APR vs. IL: Look at fee income relative to expected volatility.

- Asset quality: Reputable, audited, non-rebasing (or rebasing-aware pools).

- Protocol security: Audits, bug bounties, battle-tested contracts.

- Operational costs: Gas, rebalancing frequency, external tool subscriptions.

- Incentives: Attractive but temporary. Don’t rely on emissions persisting.

- Composability: Does the LP token unlock extra yield (e.g., leverage, lending, restaking)? Stacking boosts risk.

LP Strategies by Risk Profile

- Conservative:

- Stable-stable pools (USDC/DAI), low fee tier, wide range.

- Goal: steady fees, minimal IL.

- Balanced:

- Major-major (ETH/BTC) or LST-ETH pools; moderate fee tier and range, occasional rebalancing.

- Aggressive:

- Narrow-range volatile pairs; frequent rebalancing; periodic delta-hedging with perps or options.

- Event-driven:

- Provide liquidity around known catalysts (airdrops, upgrades) when volume spikes then exit.

LPing on Centralized Exchanges (Quick Note)

On CEXs, retail can’t usually “LP” directly. Instead, professional market makers (firms or bots) provide liquidity and earn from spreads and rebates. Becoming a market maker requires:

- low-latency infrastructure,

- robust risk models,

- capital for inventory and hedging across venues.

FAQs

Is LPing passive income?

Sometimes, but not truly “set and forget.” Concentrated pools need management; even stable pools face depegs or contract upgrades.

What yields are realistic?

Yields vary widely with volume and volatility. A quiet week on a stable pool might be <5% APR; a volatile week on a high-fee pool can spike double-digits. Past yields don’t predict future returns.

What about single-sided LP?

Convenient, but the protocol often pairs or synthetically balances your asset, introducing borrowing costs or smart-contract complexity. Read the docs.

How do I avoid IL entirely?

You can’t if prices move; IL is structural to AMMs. You can minimize it (stable pairs, hedging, wider ranges) or aim to out-earn it via fees.